What is the US Hemp Derivatives Market Overview – definition, scope, and significance?

The US Hemp Derivatives Market encompasses all products that are extracted or processed from industrial hemp (Cannabis sativa L.) cultivated in the United States. It includes three primary types – hemp‑derived CBD, hemp seed oil, and hemp fiber – and serves a wide range of applications such as food and beverages, pharmaceuticals, and personal care. The market’s significance lies in its dual role as a driver of agricultural diversification and a catalyst for novel product development in high‑growth sectors. With a 2026 market size of US 6.54 billion, the industry reflects strong consumer interest in natural, plant‑based ingredients and the regulatory shift that legalized hemp cultivation after the 2018 Farm Bill.

What are the main drivers, restraints, challenges, and opportunities shaping the US Hemp Derivatives Market?

Key drivers include the expanding consumer preference for wellness‑focused products, the therapeutic potential of cannabidiol (CBD), and increasing mainstream acceptance of hemp‑based foods. Opportunities arise from untapped applications in cosmetics, functional beverages, and emerging biotech uses of hemp fiber. Restraints involve a fragmented regulatory environment, especially concerning CBD’s classification, which can limit product labeling and interstate commerce. Challenges consist of supply‑chain volatility, limited large‑scale processing infrastructure, and competition from synthetic alternatives. Together, these forces create a dynamic landscape where strategic agility is essential for market participants.

What are the current growth trends in the US Hemp Derivatives Market?

Current trends show a shift from niche, specialty products to mass‑market offerings. Hemp‑derived CBD is moving beyond dietary supplements into regulated pharmaceutical pipelines, while hemp seed oil is gaining traction as a “superfood” ingredient in mainstream grocery aisles. Hemp fiber is being explored for sustainable packaging and automotive composites, reflecting a broader sustainability trend. Additionally, brands are pursuing clean‑label formulations and transparent sourcing, which are influencing product development and marketing strategies across all three types.

How did COVID‑19 impact the US Hemp Derivatives Market and what is the recovery trajectory?

The pandemic initially disrupted farming cycles and processing capacity, leading to temporary shortages of raw hemp material. However, heightened consumer focus on health and immunity accelerated demand for CBD and hemp‑based nutraceuticals. Online sales surged, offsetting retail closures. Post‑2020, the market rebounded quickly, with supply‑chain adjustments and increased investment in processing facilities. The recovery trajectory remains positive, supported by continued consumer confidence and the sector’s resilience to future disruptions.

Who are the major competitors and what is the level of consolidation in the US Hemp Derivatives Market?

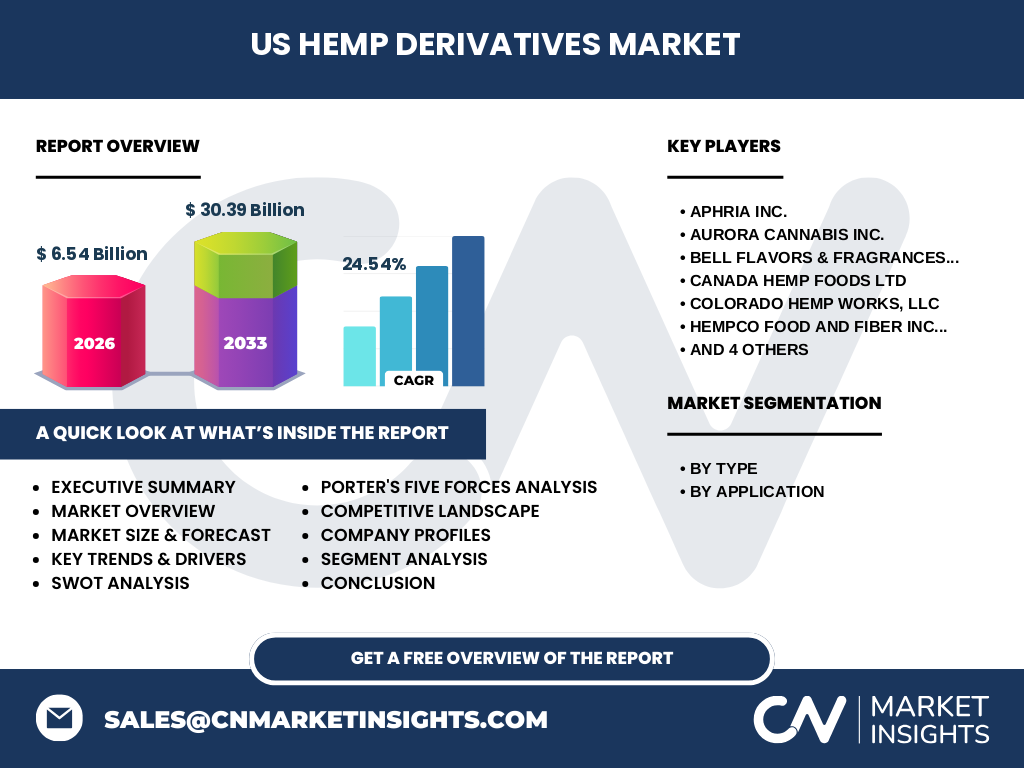

The competitive landscape features a mix of large multinational cannabis operators and specialized hemp processors. Leading players include Aphria Inc., Aurora Cannabis Inc., Bell Flavors & Fragrances Inc., Canada Hemp Foods Ltd, Colorado Hemp Works, LLC, Hempco Food and Fiber Inc., Neptune Wellness Solutions, Inc., Radient Technologies, Re Botanicals, Inc., and Z‑Company BV. While the market is still relatively fragmented, recent strategic alliances and acquisitions indicate a gradual consolidation trend aimed at securing supply chains, expanding product portfolios, and achieving economies of scale.

What are the key findings highlighted in the Executive Summary?

The Executive Summary underscores a robust growth outlook, driven by a 24.54% CAGR projected from 2027 to 2033, expanding the market from US 6.54 billion in 2026 to US 30.39 billion by 2033. Growth is propelled by diversified applications, regulatory encouragement, and strong consumer demand. Competitive dynamics point to increasing consolidation, while opportunities abound in sustainable packaging, pharma‑grade CBD, and functional foods. Investors are advised to focus on companies with integrated supply‑chain capabilities and innovative product pipelines.

What is the forecast for the US Hemp Derivatives Market from 2025 to 2032?

Based on the provided CAGR of 24.54%, the market is expected to maintain rapid expansion throughout the forecast horizon. By 2027, the market will surpass US 10 billion, and continued compound growth will lead to an estimated US 30.39 billion by 2033. This trajectory reflects sustained adoption across food, pharma, and personal‑care segments, as well as the scaling of processing infrastructure and the entry of new entrants capitalizing on the sector’s profitability.

How is the US Hemp Derivatives Market sized and shared by segment?

The market is segmented by type—hemp‑derived CBD, hemp seed oil, and hemp fiber—and by application—food and beverages, pharmaceuticals, and personal care. While exact monetary splits are not disclosed, the prominence of CBD in pharmaceuticals and personal‑care indicates a high‑value segment, whereas hemp seed oil drives volume in food and beverages. Hemp fiber, though smaller in current revenue, holds strategic importance due to its sustainability potential.

What does the global US Hemp Derivatives Market size and share look like by region?

Globally, the United States represents the largest consumer and producer of hemp derivatives, accounting for the full market size of US 6.54 billion in 2026. International comparisons show the US leading in both cultivation acreage and processed product output, positioning it as a benchmark for regulatory frameworks and market development.

What are the regional performance highlights within the US Hemp Derivatives Market?

Key regions include the Pacific Northwest, Colorado, and Kentucky, where climate and legislative support favor large‑scale hemp farming. The West Coast exhibits strong demand for hemp‑based foods and cosmetics, while the Midwest focuses on fiber and seed oil production for industrial applications. Regional analysis reveals that proximity to processing hubs reduces logistics costs and enhances market responsiveness.

Which companies lead the US Hemp Derivatives Market and what are their core strategies?

Top companies such as Aphria Inc. and Aurora Cannabis Inc. leverage vertical integration—controlling cultivation, extraction, and distribution—to ensure product consistency. Bell Flavors & Fragrances Inc. focuses on specialty extracts for the personal‑care sector, while Canada Hemp Foods Ltd emphasizes organic, clean‑label food products. Neptune Wellness Solutions, Inc. pursues a diversified portfolio across CBD, nutraceuticals, and consumer goods, and Radient Technologies invests heavily in advanced extraction technologies to improve yield and purity.

How does Porter’s Five Forces analysis apply to the US Hemp Derivatives Market?

Threat of new entrants is moderate; low entry barriers for small growers are offset by high capital requirements for processing. Bargaining power of suppliers is moderate, as a limited number of certified processors control raw material pricing. Bargaining power of buyers is high, given abundant product choices and price sensitivity. Threat of substitutes remains low to moderate, with synthetic cannabinoids offering limited functional equivalence. Industry rivalry is intense, driven by aggressive branding, product innovation, and strategic partnerships.

What are the SWOT insights for the US Hemp Derivatives Market?

Strengths: strong consumer demand, legal farm bill support, diversified applications. Weaknesses: regulatory uncertainty around CBD, fragmented supply chain. Opportunities: expansion into pharma‑grade CBD, sustainable packaging using hemp fiber, international export growth. Threats: potential tightening of federal regulations, competition from synthetic alternatives, supply volatility due to climate impacts.

How is value created and transferred in the US Hemp Derivatives value chain?

The value chain begins with seed selection and cultivation, followed by harvesting, drying, and transportation to processing facilities. Extraction (for CBD) or cold‑pressing (for seed oil) creates the primary derivative, which is then refined, tested, and formulated into end products. Distribution channels include e‑commerce platforms, specialty retailers, and mainstream grocery and pharmacy chains. Ancillary services such as certification, third‑party testing, and marketing add further value.

What investment insights are most relevant for stakeholders in the US Hemp Derivatives Market?

Investors should prioritize companies with integrated operations that mitigate supply‑chain risk, and those investing in proprietary extraction or fiber‑processing technologies. Strategic capital allocation to scalable processing facilities can capture economies of scale as demand rises. Partnerships with food and pharma firms accelerate market entry for new applications. Monitoring regulatory developments remains essential to manage compliance risk.

What are the concluding takeaways for the US Hemp Derivatives Market?

The market is poised for exponential growth, driven by a 24.54% CAGR and a projected US 30.39 billion valuation by 2033. Success will hinge on navigating regulatory nuances, securing reliable supply, and innovating across product categories. Companies that can harmonize agriculture, technology, and consumer branding are likely to capture the largest share of this burgeoning sector.

How was the research conducted for this market report?

Research methodology combined primary interviews with industry experts, secondary data collection from company filings, regulatory documents, and reputable market databases. Trend analysis, financial modeling, and scenario forecasting were employed to derive the CAGR and market size projections. Competitive intelligence was gathered through publicly available information and supplier surveys.

What is the scope of this market research?

The scope covers the United States hemp derivatives ecosystem, focusing on three product types (CBD, seed oil, fiber) and three applications (food & beverages, pharmaceuticals, personal care). Temporal coverage spans 2026 baseline data through a 2027‑2033 forecast. Geographic focus remains on the US, with global context limited to the US’s share of the worldwide market.

Which key companies have made recent developments in the US Hemp Derivatives Market?

Recent developments include Aphria Inc.’s acquisition of a processing plant in Colorado to increase CBD output, Aurora Cannabis Inc.’s partnership with a major pharmacy chain for pharma‑grade CBD distribution, Bell Flavors & Fragrances Inc.’s launch of a new natural fragrance line derived from hemp oil, and Neptune Wellness Solutions, Inc.’s introduction of a fortified hemp‑seed‑oil beverage. Radient Technologies announced an upgraded extraction system that improves cannabinoid purity, while Re Botanicals, Inc. unveiled a personal‑care line emphasizing sustainable hemp fiber packaging.